Table of Contents

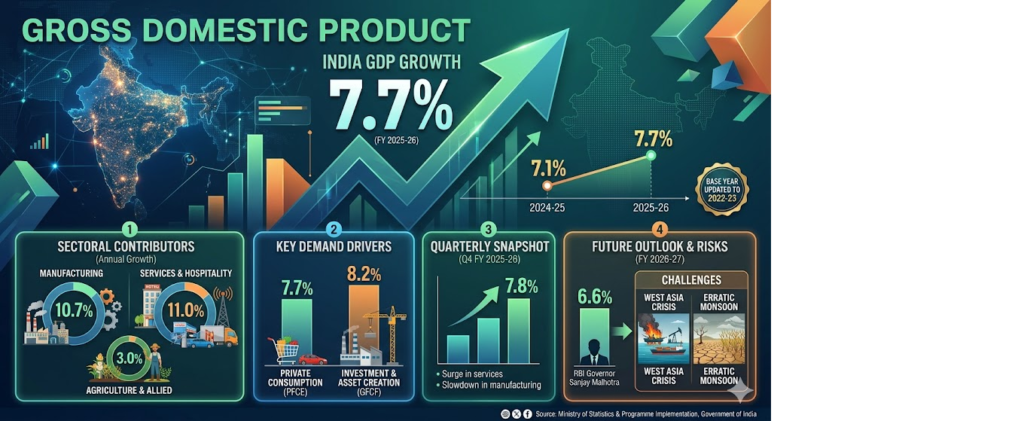

The Ministry of Statistics and Programme Implementation (MoSPI) has released the provisional estimates of Gross Domestic Product (GDP) for the financial year 2025-26.

Key Highlights of the Data

- Annual GDP Growth: India’s real GDP growth accelerated to 7.7% in FY 2025-26, up from 7.1% recorded in FY 2024-25. This surpasses the advance estimate of 7.6% projected in February 2026.

- Quarterly Performance: The fourth quarter (Q4) of FY 2025-26 registered a robust growth rate of 7.8%.

- Methodological Update: The government has updated the GDP base year to 2022-23 and introduced improved calculation methodologies to better capture structural shifts in the economy.

- Future Outlook (FY 2026-27): The Reserve Bank of India (RBI) projects growth to moderate to 6.6% in the upcoming fiscal year, citing global and climatic headwinds.

Sector-wise Performance Analysis

| Sector | FY 2024-25 Growth | FY 2025-26 Growth | Key Observations / Dynamics |

| Manufacturing | 9.3% | 10.7% | Hit double-digit growth annually, driven by structural reforms. However, a sharp deceleration was noted in Q4 (falling to 7.3% from 11.8% in Q4 of FY24), indicating cooling momentum at the end of the fiscal year. |

| Services (Trade, Hotels, Transport, Comm.) | 6.6% | 11.0% | Emerged as a major growth driver with a massive spike. Q4 growth surged to 12.4% (compared to 6.3% in Q4 FY24), reflecting resilient urban and contact-intensive services demand. |

| Agriculture & Allied Activities | 4.2% | 3.0% | Decelerated due to erratic climatic factors. Q4 growth stood at 3.6%, highlighting the ongoing vulnerability of the primary sector to monsoon fluctuations. |

Key Demand-Side Components of GDP

- Private Final Consumption Expenditure (PFCE): Quickened significantly to 7.7% in FY 2025-26 from 5.8% in the previous fiscal. This indicates a strong revival in domestic household demand and consumer confidence.

- Gross Fixed Capital Formation (GFCF): Grew by 8.2% in FY 2025-26 compared to 6.4% in FY 2024-25. This underscores a robust pace of asset creation, fueled by both public infrastructure push and reviving private capital expenditure (CapEx).

Despite a stellar performance in FY26, economists and policymakers note that growth is expected to cool down due to the following factors:

Key Challenges and Downside Risks for FY 2026-27

- Geopolitical Vulnerabilities: The ongoing crisis in West Asia threatens global supply chains, impacting logistics cost and energy prices.

- Climatic Uncertainties: The possibility of a lower-than-normal monsoon poses severe risks to food inflation and rural demand, which could drag down overall consumption.

- Decelerating Industrial Momentum: The visible cooling off in manufacturing growth during Q4 indicates potential capacity constraints or rising input costs that need tracking.

Prelims Type Question

Q. Consider the following statements with reference to the Provisional Estimates of GDP for FY 2025-26 released by MoSPI:

- India’s annual real GDP growth for FY 2025-26 accelerated past 7.5%.

- The Manufacturing sector maintained an identical growth rate in Q4 of FY 2025-26 compared to the corresponding quarter of the previous fiscal.

- Both Private Final Consumption Expenditure (PFCE) and Gross Fixed Capital Formation (GFCF) recorded higher growth rates in FY 2025-26 than in FY 2024-25.

Which of the statements given above are correct?

(a) 1 and 2 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

Answer: (c)

- Explanation: Statement 1 is correct as the annual growth stood at 7.7%. Statement 2 is incorrect because the manufacturing sector decelerated sharply in Q4 of FY25-26 to 7.3% from 11.8% in Q4 of FY24-25. Statement 3 is correct as PFCE accelerated to 7.7% (from 5.8%) and GFCF grew to 8.2% (from 6.4%).

Mains Type Question

Q. Discuss the structural drivers behind India’s 7.7% GDP growth in FY 2025-26. Despite this resilient performance, what are the emerging macroeconomic headwinds that justify a conservative growth forecast for FY 2026-27? (150 Words, 10 Marks)

Model Framework:

- Introduction: Acknowledge the provisional estimates showing 7.7% growth in FY25-26, highlighting the economy’s resilience despite global volatility.

- Body Paragraph 1 (Drivers): Explain structural factors like the double-digit expansion in Manufacturing (10.7%) and contact-intensive Services (11%). Mention demand-side triggers: revival in consumer spending (PFCE at 7.7%) and strong investment/asset creation via GFCF (8.2%).

- Body Paragraph 2 (Headwinds): Detail why growth is expected to moderate to 6.6% next year. Focus on supply shocks from West Asia impacting fuel/trade routes, agriculture vulnerability due to projections of a below-normal monsoon, and the visible slowing down of late manufacturing activity in Q4.

- Conclusion: Conclude by highlighting the need for structural reforms to improve “Ease of Doing Business” and buffer the domestic economy from global geopolitical and climate vulnerabilities.